No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

As mortgage experts, we are big fans of VA loans. With this program, a veteran can buy a home with no down payment, rates lower than for conventional loans, and no mortgage insurance.

This means that a veteran buyer can buy a home with a lower payment than if he or she used a conventional loan.

What most people don’t know, however, is that the underwriting standards for getting a VA loan approved are very different—and much easier—than for other loan programs. VA loans use a completely different (some would say more sensible) method of evaluating the veteran’s ability to qualify for the loan. This may also mean being able to qualify for more home.

Please note: What you are about to read is somewhat technical. It also uses something that, for many, is an instrument of torture: math. Stick with us, though. We promise it will be worth your pain and suffering.

Lenders approve most loans by calculating a number called the Debt To Income Ratio (DTI). They add up the total housing expense (mortgage payment plus taxes, insurance and homeowner’s association dues and mortgage insurance, if any) and all other debt payments. That number, the Total Debt, is then divided by the borrower’s total gross income (how much money he made) before taxes to arrive at the DTI.

A borrower with monthly income of $6,000 and total debt of $2,400 would have a DTI of 40%. Conventional loans allow a maximum DTI of 45%. Under these guidelines, a buyer earning $6,000 a month, with $250 per month in debt payments, making a 5% down payment would qualify to buy a home for about $325,000.

We qualify VA buyers using the “Residual Income” method. We need to know that the veteran buyer has enough money left over after making the house payment and paying other obligations to support a reasonable lifestyle.

The Department of Veterans Affairs (the VA) provides a form: the Loan Analysis. If you want to look under the hood, you can find it here. Here’s how it works:

We first calculate the total house payment, including taxes, insurance, homeowner’s association dues (if any) and maintenance and utilities. VA assumes that those costs will amount to $0.14 per foot. A 1,200 square foot home will have utilities and maintenance of $168/mo. If the veteran is buying a home for $490,000, his total housing expense is $2,933. If he has $250 in monthly payments (car, credit cards, etc.), his total debt is $3,183.

If the veteran buyer has a salary of $6,000, his take-home (net) pay will be about $4,500, depending on how many exemptions and deductions he claims on his tax return. We subtract the total debt ($3,183) from his net income to get Residual Income of $1,317.

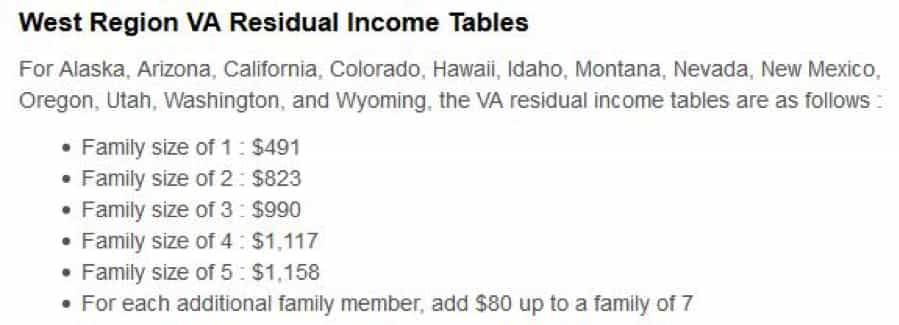

VA publishes guidelines for Residual Income in different areas of the country and for different family sizes. In the West Region, the guidelines look like this:

This means that our veteran buyer’s family will qualify for this loan easily—if they are a family of four, they have more than the required $1,117 left over each month.

To put this into perspective, if this were a conventional loan, the DTI would be over 50%—far too high for a conventional loan. Where this veteran will qualify to buy a $490,000 home with no down payment, the same borrower would be limited to $325,000 if he used conventional financing with a 5% down payment.

There are some who might say that approving a loan with no down payment and such a high DTI is risky; the fact is that VA loans, even during the difficult times following the 2008 financial crisis, have had a lower rate of delinquency and default than conventional loans.

The VA home loan program has helped millions of men and women since 1944 who have served their county in the military to become homeowners. This unique (but realistic) method of evaluating and approving these loans makes home ownership closer than ever.

Interested in applying for a VA loan? You can do so now through our secure online portal with no charges and no obligations.

Are you interested in applying for a VA loan to buy a home? Sammamish Mortgage can help. We are a local, family-owned company based in Bellevue, Washington. We serve the entire state, as well as the broader Pacific Northwest Region including OR, CO & ID. We offer a variety of mortgage programs to suit your particular situation. Please contact us if you have mortgage-related questions.

Whether you’re buying a home or ready to refinance, our professionals can help.

{hours_open} - {hours_closed} Pacific

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.