States We Lend In

Our loan officers are ready and waiting to help you apply for your home loan.

Many would-be homebuyers are still sitting on the fence wondering if they should buy a home now or wait until their finances are a little stronger. Does that sound like you?

Maybe you’re giving yourself more time to save up for a bigger down payment. Or perhaps you’re waiting until you’ve got a better job, get a raise, or paid down some of your debts. While that’s wise to some degree, it may not be so wise to wait too long, as waiting to buy a home could cost you.

It’s no secret that home prices are through the roof these days. The average price for a home has skyrocketed across much of the country. But the truth is, real estate prices will always increase over time.

Even if the rate of increase may slow down and even plateau from time to time, prices only go in one direction over time: up.

Let’s look at a few examples of home price appreciation over the past 12 months in the Pacific Northwest, according to real estate research firm Zillow:

From the figures above, it’s clear to see that the [past year has seen extraordinary price increases. Anyone who bought a home last year or before has been able to get into the market before price increases forced their monthly mortgage payments to increase.

At the same time, they’ve been able to take advantage of price appreciation and build home equity quickly.

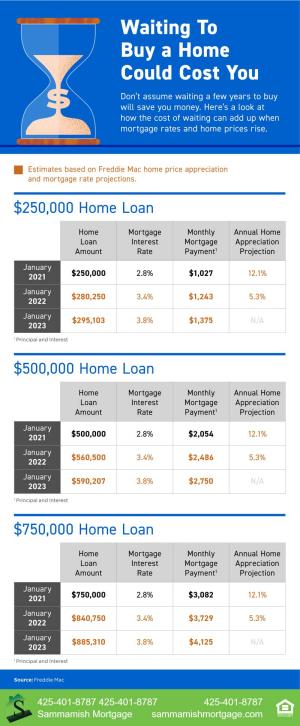

Don’t assume that waiting a few years to buy a home will save you money. Here’s a look at how the cost of waiting can add up when mortgage rates and home prices rise.

The following estimates are based on Freddie Mac’s home price appreciation and mortgage rate projections.

Let’s say you take out a home loan in January 2021 for $250,000 at a mortgage interest rate of 2.8% on a 30-year fixed-rate mortgage. Your monthly mortgage payments would work out to be $1,027.

Over the next 12 months, home prices increase, which means you would have had to take out a home loan of $280,250 based on that rate of price increases.

Based on the new home loan amount of $280,250 and a higher mortgage interest rate of 3.4%, your monthly mortgage payment would now be $1,243. Let’s say that the price of homes appreciates again at a rate of 5.3%.

That means that by January 2023, you would now have to take out a $295,103 home loan. At a mortgage interest rate of 3.8%, your mortgage payments would work out to be $1,375.

As you can see, just waiting 2 years means you’re paying roughly an additional $350 more per month than you would have if you purchased a home in January 2021 instead of waiting until January 2023.

As you would imagine, the increase in mortgage cost would rise significantly if your home loan amount was much higher.

Let’s now use an example of a $750,000 home loan using the same mortgage interest rate increases and home price appreciation rates. If you were to take out a $750,000 home loan in January 2021, your mortgage payments would work out to be $3,082.

But if you wait one year, your mortgage payments would jump to $3,729 per month. And if you wait another year, your mortgage payments would spike to $4,125.

In this case, waiting just 2 years means you’d be paying more than $1,100 more per month in mortgage payments.

When you take out a mortgage, you’ll need to have a sizable down payment to put toward the purchase price of the home. And perhaps you’re waiting until you’ve built up a certain amount so you can keep your loan amount low. But at the same time, you could be setting yourself up for a much more expensive mortgage.

The calculations above based on homer price and mortgage interest rate projections paint a picture of much higher monthly mortgage obligations. Those hundreds of extra dollars that you would be spending by waiting to buy a home could be spent in different ways, including investing.

And when you tally up all that extra money spent each month, you’d be shocked at how much that would come to at the end of the year, and even over multiple years. It could add up to be a huge amount of money.

If you think you’re not ready to buy a home right now, consider purchasing a property and renting it out for the first little while to help you out financially. As we’ve already shown you, waiting to buy a home can put you in a position to spend way more than you would have bought today.

But rather than be stuck paying a mortgage on your own, perhaps buying a home and renting it out can help. Every rent check you collect can go towards paying your mortgage. In the meantime, you’re building equity in the home and avoiding the trap of getting stuck with high home prices and mortgage interest rates in the future.

Buying a home is a big deal. But it’s also a sound investment. With the right team behind you, you can get into the market today before prices and rates continue increasing, saving you a lot of money in the long run.

Sammamish Mortgage is a local lending firm serving the broader Pacific Northwest region, including Washington state, Idaho, Colorado, and Oregon. We are proud to offer a wide variety of mortgage programs and products with flexible qualification criteria since 1992. Please contact us if you have any questions or are ready to apply for a home loan.

Our loan officers are ready and waiting to help you apply for your home loan.

Learn more about the people behind Sammamish Mortgage

Whether you’re buying a home or ready to refinance, our professionals can help.

Mortgage Support — 24/7

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

Adjust the parameters based on what you want to track