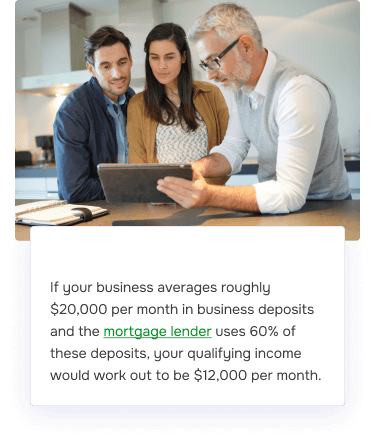

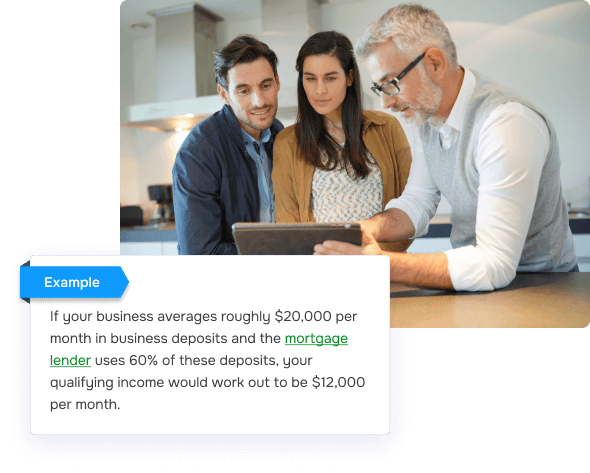

What Is a Bank Statement Loan?

A bank statement loan is a type of mortgage designed for self-employed individuals who may have difficulty getting approved for a conventional loan because of their non-traditional income reporting.

Typically, mortgage applicants use documents such as W-2s, pay stubs, or tax returns when applying for a home loan. However, these documents often don’t always accurately reflect a self-employed individual’s actual earnings. Business write-offs and deductions typically come into play that can skew income.

Instead, self-employed individuals can use personal or business bank statements to depict their average income.