States We Lend In

Our loan officers are ready and waiting to help you apply for your home loan.

What are the biggest reasons why renters eventually choose to buy?

Many people rent rather than purchase a home because of their financial circumstances. Maybe they’ve got a lot of debt on their plate that they’re working through to pay off, such as student loans, while their incomes are not high enough to put some money aside every month to save up for a down payment.

Or maybe renters believe they’ll have more flexibility to move without being tied down to a house that they’d first need to sell before moving.

For some households, renting is the better fit for now. But many renters eventually decide to buy because homeownership can offer more payment stability, a chance to build equity over time, and more control over the living space. The key is making sure buying matches your budget, timeline, and comfort with the responsibilities that come with owning a home.

What are the reasons why renters buy?

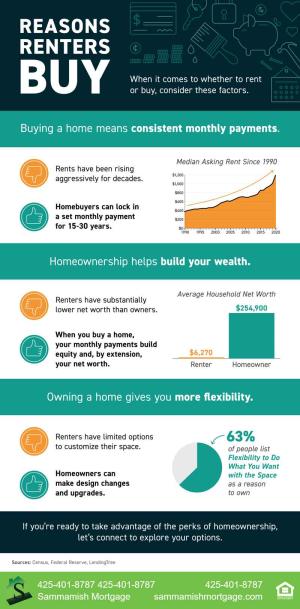

When it comes to whether to rent or buy, consider these factors.

One of the biggest reasons renters buy is to gain more predictability in their housing payment. With a fixed-rate mortgage, the principal and interest portion of the payment is generally stable, which can make long-term budgeting easier than renting in a market where lease costs may rise over time.

That said, owning does not mean every housing cost stays the same. Property taxes, homeowners insurance, HOA dues, maintenance, repairs, and utilities can all change. So while a fixed-rate mortgage can create more payment stability, it does not guarantee a fully fixed total monthly housing cost.

Renting can still be simpler in the short term, especially if you want fewer surprise expenses or expect to move soon. But for renters who want a more predictable base payment over time, buying can be appealing.

By owning, you may gain more payment stability over time, especially if you plan to stay put and choose a fixed-rate loan.

| Factor | Renting | Buying |

|---|---|---|

| Payment predictability | Lease payments may rise at renewal | Fixed-rate mortgage principal and interest are generally more stable |

| Equity | No ownership stake in the property | May build home equity over time |

| Upfront costs | Usually lower upfront cash needs | Typically requires down payment, closing costs, and reserves |

| Maintenance responsibility | Often handled by landlord | Usually handled by homeowner |

| Flexibility to move | Often easier to relocate after lease ends | Better suited to buyers planning to stay for a while |

| Ability to customize | Usually limited by lease terms | More control over updates and improvements |

Another reason renters buy homes is the potential to build equity over time. Unlike rent, which does not create ownership in the property, mortgage payments can gradually increase your stake in the home, and your equity may also grow if the home’s value rises.

That does not make homeownership a guaranteed wealth-building strategy in every situation. Outcomes depend on how long you stay in the home, the price you pay, loan terms, ongoing ownership costs, and market conditions. Still, for buyers who keep a home long enough, ownership can become an important part of long-term finances.

The gap between renters and homeowners is often reflected in broader net worth data. According to the most recent Federal Reserve Survey of Consumer Finances, 2022 is the latest survey year, and the typical U.S. homeowner has a net worth of $430,000. That does not mean buying a home automatically creates that result, but it does show why homeownership is often part of long-term wealth-building conversations.

If you ever sell your home in the future, you may be able to benefit from the equity you’ve built. And if you keep your home over the years, you can use your home equity as a potential financial resource later on.

Owning a home gives you more control over your space. As a homeowner, there’s no landlord setting rules about paint colors, fixtures, or certain upgrades. If you want to change your garage door, update a room, or make other design improvements, you typically have more freedom to do so because you own the property.

That kind of flexibility is different from mobility. Renters often have an easier time relocating, especially after a lease ends. Buying is usually a better fit for people who want more control over the home itself and expect to stay long enough for ownership to make sense.

If personalizing your living space matters to you, that can be a meaningful reason to buy instead of rent.

Buying may be a better fit than renting if most of these statements sound true for your situation:

If several of these do not apply yet, renting may still be the better choice for now. Buying tends to work best when it supports your broader financial and lifestyle goals.

Sammamish Mortgage can help. We serve clients across Washington, Idaho, Colorado, Oregon, and California. Since 1992, we’ve been providing several mortgage programs and products with flexible qualification criteria to borrowers across the Pacific Northwest. Visit our website to get an instant rate quote or to use our online mortgage calculator. Or, reach out to us if you are ready to get pre-approved for a mortgage.

No. Buying is not always cheaper, especially when you include property taxes, insurance, maintenance, HOA dues, and upfront costs. For some households, renting costs less or offers better short-term flexibility.

Common reasons include more payment stability with a fixed-rate mortgage, the potential to build equity, more control over the home, and the desire to settle into a place long term.

In general, buying tends to make more sense when you expect to stay put for a reasonable period. A longer time horizon can give you more opportunity to recover upfront costs and benefit from ownership.

Yes. Some buyers move forward with less than 20% down, depending on the loan program and their financial profile. The bigger question is whether the full monthly payment and upfront costs fit comfortably within your budget.

Many renters focus on the mortgage payment alone and forget about property taxes, homeowners insurance, HOA dues, maintenance, repairs, and utility differences.

You’re generally in a stronger position when you have stable income, manageable debt, enough cash for upfront costs and reserves, and a payment that fits your budget beyond just principal and interest.

Buying often makes more sense when you have stable finances, can handle the full cost of ownership, and plan to stay in the home long enough for the upfront costs and responsibilities to be worthwhile.

Many people buy because they want more long-term payment predictability, the chance to build equity, greater control over their living space, and more stability if they plan to stay put.

It depends on your income, savings, debt, expected time in the home, and total housing costs. Renting may be better for flexibility and lower upfront expenses, while buying may help with payment stability and equity over time.

It can be. Homeownership usually gives you more freedom to personalize the property with updates and improvements, which can be a major advantage for people who value control over their living space.

Our loan officers are ready and waiting to help you apply for your home loan.

Learn more about the people behind Sammamish Mortgage

Whether you’re buying a home or ready to refinance, our professionals can help.

Mortgage Support — 24/7

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

Adjust the parameters based on what you want to track