States We Lend In

Our loan officers are ready and waiting to help you apply for your home loan.

The mortgage application process may seem like a daunting task, but it doesn’t have to be. As long as you go into the process knowing everything you need to know, there’s little reason why you shouldn’t find success.

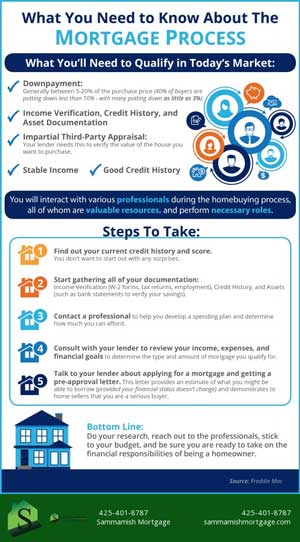

Down payment. You won’t have to come up with the entire purchase amount in full when you buy a house, but you will need some for of down payment (unless you qualify for a VA loan). The down payment amount required will depend on the type of home loan you take out and your financial health. Generally speaking, you can expect to pay anywhere from 3% to 20% of the purchase price of the home or more for a down payment.

Income verification, credit history, and asset documentation. Your lender will want to know how much you earn, what your credit score is, and what assets you currently have before determining whether or not you are eligible for a mortgage. Find out what your current credit score is so you know how strong your profile is before going into the application process. Start collecting all of your documentation, including your pay stubs, tax forms, and letter of employment.

Your debt-to-income ratio is another qualification factor that lenders review alongside your income, credit, and assets. This ratio compares your monthly debt obligations to your income and helps show whether your finances can support a mortgage payment.

Third-party appraisal. The lender will also want to know what the value of the home is that you intend to buy, and an appraisal will be ordered to find this out. This will provide the lender with information that will help determine an appropriate loan amount to approve you for.

Stable income. Your income will need to be adequate enough to cover your mortgage payments, plus all your other current debt obligations.

Good credit history. A high credit score will mean you’d be less of a risk for the lender because you’ll be less likely to default on your home loan.

The mortgage process generally moves through several stages, starting with qualification and preparation, then moving into lender discussions and application steps. Understanding these stages can make the process feel more organized and help you know what to expect as you move from reviewing your finances to applying for a loan.

To make sure you go through the mortgage process in full and increase your chances of approval, take the following steps:

After pre-approval and application, the mortgage process continues with underwriting and closing. During this part of the process, the lender completes its review of the loan file and finalizes the remaining steps needed before the mortgage can be completed.

Get in touch with a financial professional to help you understand how much you can afford, and consult with your lender to find out what type of mortgage might be best suited for you. Finally, talk to your mortgage lender about getting pre-approved for a mortgage and applying for a specific home loan. Get in touch with Sammamish Mortgage to learn more!

Sammamish Mortgage is a local lending firm serving the broader Pacific Northwest region including Washington state, Idaho, Colorado, California, and Oregon. We are proud to offer a wide variety of mortgage programs and products with flexible qualification criteria. Please contact us if you have any questions or are ready to apply for a home loan.

Most lenders review your down payment, income, credit history, assets, employment, existing debts, and the appraised value of the home.

The amount depends on the loan program and your financial profile. Many buyers put down between 3% and 20% of the home’s purchase price, while some loan options may require more or less.

No. Some loan programs, such as eligible VA loans, may allow qualified borrowers to buy a home with no down payment.

Lenders verify income to confirm that you have enough stable earnings to manage monthly mortgage payments along with your other debt obligations.

Common documents include recent pay stubs, tax forms, employment verification, bank statements, and records of assets and debts.

Your credit score helps lenders measure borrowing risk. A stronger credit profile can improve your chances of approval and may help you qualify for better loan terms.

A third-party appraisal is an independent estimate of the home’s market value. Lenders use it to help determine whether the property supports the requested loan amount.

Check your credit score, gather financial documents, review your budget, speak with a mortgage professional, and discuss loan options with a lender.

Mortgage pre-approval is a lender’s preliminary review of your finances to estimate how much you may be able to borrow, subject to final underwriting and property review.

Yes. Speaking with a lender early can help you understand your budget, compare loan options, and identify any financial issues that should be addressed before you make an offer.

Our loan officers are ready and waiting to help you apply for your home loan.

Whether you’re buying a home or ready to refinance, our professionals can help.

Mortgage Support — 24/7

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

Adjust the parameters based on what you want to track