States We Lend In

Our loan officers are ready and waiting to help you apply for your home loan.

Wondering what credit score is needed to get a home mortgage in Washington State? Sammamish Mortgage’s educational approach to lending makes us a leader in the financial space, as we help would-be homeowners learn more about how to improve their credit, manage their finances, and increase their personal wealth.

Our company was recently featured on BadCredit.Org to showcase how we support hopeful borrowers from the early stages of the homebuying process to closing and beyond, assisting consumers with everything from raising their credit score to finding the perfect loan for their needs.

Here’s everything you need to know about what a good credit score is, and how to make it even better so you can qualify for a home loan and buy that house you’ve been wishing for.

There are many factors that play a role in your ability to secure a mortgage, and your credit score is one of them. But what constitutes a “good” credit score? This article will explain more.

Whether we like it or not, our FICO scores have an effect on our lives.

What is this mysterious three-digit number, how does it affect us, and how can we make it as good as it can be?

The acronym FICO comes from “Fair, Isaac and Company,” the organization that created the credit scoring system in 1956. Widespread use among creditors began in 1989. Today, the most common version of the FICO score ranges between 300 and 850.

There are three major credit repositories (credit bureaus) that collect information about how consumers handle their financial obligations. A credit report lists “open trade lines” (active accounts), closed accounts in good standing as far back as ten years, payment history, and derogatory information. This last category includes late payments, collection accounts, charge-offs and public record items such as judgments, liens, bankruptcies and foreclosures.

The FICO models—and there are several of them—consider all the information on the consumer’s credit report and generate a three-digit number called the FICO score.

Most consumers have three FICO scores, one from each of the three credit bureaus (Experian, Equifax and TransUnion). The scores vary a bit between the bureaus because of slight differences between the versions of FICO each of them uses and the different account information they might report.

Lenders typically discard the high and low scores, using the remaining score which is called, logically enough, the “mid score.” If there are two or more borrowers on the loan, the lender will use the lowest mid score for its lending decision.

Conventional loans allow a FICO score as low as 620, while government-insured FHA loans are more forgiving. They allow a score as low as 585 for a loan with a 3.5% down payment.

There is a price to pay for the lower score, however. Borrowers with scores close to the allowable minimum can expect to get a rate about .75% higher than those with “good” credit scores—740 or higher.

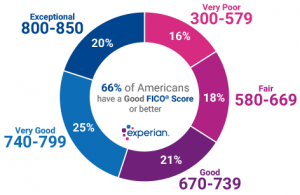

This brings us to the question of what constitutes a “good” credit score. Although “good” is somewhat vague, most people would agree that a score of around 700 is “good,” while 740 and higher is “excellent.” Experian views credit scores this way:

While a borrower with a “fair” score can get a mortgage, there are real benefits to having a higher score. Fannie Mae and Freddie Mac, the companies who buy most mortgages in the U.S. and who set the guidelines, use “risk-based pricing.”

This means that lenders look at a chart containing ranges of credit scores and ranges of loan-to-value ratios. Where those two factors intersect for a borrower, we’ll find an adjustment to their rate. A 700 score and a loan for 80% of the home’s value will have a rate about .25% higher compared to the rate for a borrower with a score of 740 or better.

Optimizing your credit score can pay real dividends. If your score is close to one of the “pricing thresholds,” an improvement of just one or two points could result in your getting an interest rate 1/8% lower or more.

Getting a higher credit score may be easier than you think. Understanding how the scoring system works is the first step. The biggest influence on your score is obvious: your credit history. It makes up 35% of your FICO score.

While we can’t remove a late payment that is accurately reported, we do have another influential item that we can change: “Amounts Owed.” This does not mean the total amount of debt you have outstanding. It means your “credit utilization.” This refers to the percentage of your credit card limits you have in outstanding balances.

If you have one credit card with a credit limit of $3,000 and a reported balance of $600, your credit utilization is 20%.

Although there is no way to know for certain how the proprietary FICO model works, we know from experience that when the balance on a credit card exceeds about 30% of the credit limit, your score begins to suffer.

If you have a maxed-out $3,000 credit card, that one account could be costing you 25 points on your score—or more. If you happen to be over the limit, the damage is greater.

The fastest way to increase your credit scores is to pay down any high credit card balances to below 30%. Paying them off altogether is best, simply because of the high interest rates charged by most credit cards.

If you have very few open trade lines (a small number of reporting accounts), you have what is called “thin” credit. This means that seemingly minor changes, such as a high balance on your single credit card, can have a larger effect on your score than if you had several open accounts.

One way to fix the “thin credit” problem is to open another account, such as a store card from a retailer or a secured card from a credit union. Having a brand new “unseasoned” account will lower your score a few points initially, but the effect is short-lived. If you have time before you plan to apply for a mortgage, this may be a useful strategy.

If your credit report shows active collection accounts, you may be able to raise your score by settling them—but be careful about the date. If the “Date of Last Activity” is two years ago or earlier, you could lower your score by paying off the account now.

The status will change from “open collection,” but two years old, to “paid collection” from the current time. Negative entries on your credit report have less effect as they get older. A 30-day late payment last month could cost you 25 points. A year from now, everything else being equal, the effect could be just 10 points. After two years, the effect is minimal.

You should be very careful about closing accounts that you have had for a long time. As accounts get older, they help your score. A ten-year-old credit card in good standing could add a dozen points to your credit score, even though you don’t use it often.

You may also be able to help your scores by increasing your credit limits on your credit cards. Issuers review accounts periodically and often increase limits automatically for consumers who consistently pay on time, but you may be able to speed up the process by requesting an increase.

Having a higher credit limit will improve your credit utilization ratio. If you have a $1,000 balance on a card with a $3,000 limit, your utilization is 33%, which could cost you a few points. If the card issuer raises your limit to $5,000, you’ve dropped to 20%, which may give you some more points.

Credit card companies hope you’ll rack up big balances so they can collect their high interest payments. That’s why they’re often happy to raise your limit. It’s a trap—don’t fall for it! Ideally, you should strive to pay your balances in full each month. You’ll save thousands of dollars that way.

Getting a higher credit score is easy—and you can get every last FICO point you’re entitled to by following these simple guidelines.

Are you curious about mortgages or are ready to apply for one? Sammamish Mortgage can help. We serve clients across Washington, Idaho, Colorado, Oregon, and California. Since 1992, we’ve been offering multiple mortgage programs with flexible qualification criteria to borrowers across the Pacific Northwest, including our Diamond Homebuyer Program, Cash Buyer Program, and Bridge Loans. Visit our website to get an instant rate quote or to use our online mortgage calculator. Or, contact us if you’re ready to get pre-approved for a mortgage.

Many conventional loans allow a minimum credit score of 620, while FHA loans may allow scores as low as 585 with a 3.5% down payment, subject to lender requirements.

A score around 700 is generally considered good, while 740 or higher is often viewed as excellent for mortgage pricing.

Yes. Borrowers with fair credit may still qualify for a mortgage, but they often receive higher interest rates and less favorable pricing than borrowers with stronger credit.

Lenders typically review credit scores from the three major credit bureaus, discard the highest and lowest scores, and use the remaining mid score. If there is more than one borrower, the lowest mid score is commonly used for the lending decision.

Mortgage pricing often uses risk-based adjustments. Lower credit scores usually mean higher perceived risk, which can lead to a higher interest rate.

Credit utilization is the percentage of available credit card limits that is currently being used. Higher utilization can lower a credit score, which may affect mortgage eligibility and pricing.

Paying down high credit card balances, keeping utilization below 30%, making all payments on time, and avoiding new negative marks can help improve a credit score before applying.

Thin credit means there are very few active accounts reporting on a credit profile. With fewer accounts, even small changes in balances or payment history can have a larger effect on the credit score.

Closing old credit cards can sometimes hurt a credit score because long-standing accounts may support credit history length and overall utilization. Keeping older accounts open may be beneficial if they are in good standing.

It can help if the higher limit lowers overall credit utilization. A lower utilization ratio may improve a credit score, provided balances are managed responsibly.

Our loan officers are ready and waiting to help you apply for your home loan.

Whether you’re buying a home or ready to refinance, our professionals can help.

Mortgage Support — 24/7

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

Adjust the parameters based on what you want to track