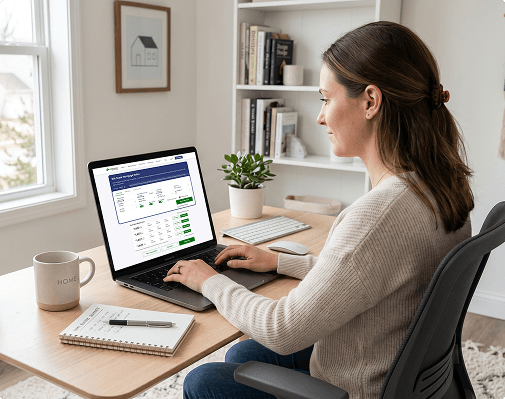

$

3,646

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.125%

6.358%

2.279

$17,011

$

3,743

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.375%

6.492%

1.060

$9,697

$

3,842

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.625%

6.653%

0.142

$4,189

$

3,646

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.125%

6.358%

2.279

$17,011

$

3,694

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.250%

6.417%

1.594

$12,901

$

3,743

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.375%

6.492%

1.060

$9,697

$

3,792

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.500%

6.571%

0.587

$6,859

$

3,842

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.625%

6.653%

0.142

$4,189

$

3,892

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.750%

6.765%

-0.413

$859

$

3,942

The monthly payment shown is principal and interest only and doesn’t include property taxes and homeowners insurance.

/mo

6.875%

6.890%

-0.556

$0

Rates Last Updated 7/30/2026, 1:02 PM

See more rates

Jul 30, 2026