States We Lend In

Our loan officers are ready and waiting to help you apply for your home loan.

Owning real estate for investment purposes is a great way to build wealth over time and even to earn a healthy income. Here are some considerations you should make when investing in rental property in WA State.

It’s no secret that many people have made a lot of money—fortunes, even—by investing in real estate. This is not to say owning rental property is a surefire path to riches, but real estate has always performed very well when compared to other investments.

There is a lot to know about investing in residential income property in WA. Here are a few of the most important aspects.

This simply means that using a little of your own money (the down payment) and a lot of someone else’s money (a mortgage), you can multiply the effect of the property’s appreciation over time. With a mortgage, your equity will increase at a rate faster than the property’s value.

Here’s a simple example: you buy a rental house for $400,000 with a 25% down payment—$100,000 cash and a $300,000 mortgage. Over some period of time, the property’s value increases to $450,000—an increase of 12.5%. The equity has increased by a little more than $50,000, as well, growing from $100,000 to $172,000—an increase of 72%.

Here’s what it looks like year-by-year:

Financing a rental property generally comes with different requirements than financing a primary residence. Buyers should be prepared for lender qualification standards, down payment expectations, and loan terms that are specific to investment properties. Understanding these financing requirements early can help set realistic expectations and shape the overall investment plan.

When you buy income property, the rent paid by the tenant offsets some or all of the mortgage payment, taxes and other expenses. With today’s low rates, it is possible to have a comparatively small down payment (25%) and still collect enough rent to cover the mortgage payment and expenses.

Before buying a rental property, it is important to review expected operating expenses and compare them to anticipated rental income. A basic cash flow analysis helps show whether the property is likely to break even, generate positive monthly income, or require out-of-pocket support. Looking closely at these numbers can make it easier to evaluate whether a property fits your goals.

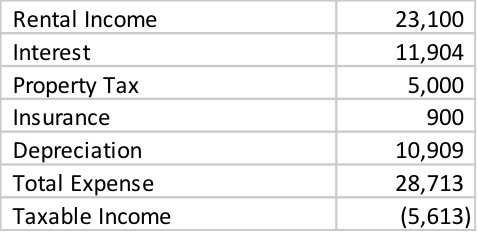

When you file your tax return, you will claim the income and expenses on Schedule E of your return. The rents you collected for the year, minus operating expenses, mortgage interest and depreciation, will give your Total Rental Real Estate Income (or loss). That’s what you’ll pay tax on.

You will be able to claim a type of expense called “depreciation.” This is the theoretical loss in value over time. For residential rental property, you can claim that “paper loss” over 27 ½ years. You depreciate only the building, not the land, so if you buy a rental house for $400,000 and the building is worth $300,000 (the appraisal will tell you the value), you will depreciate the building by $10,900 per year.

This will turn your “break-even” rental house into a positive cash flow investment, because you will now show a paper loss, even though the rental income paid for the mortgage and all the expenses of the property.

Here’s what that looks like on paper:

In this example, the property had a “paper” loss of $5,613 because of depreciation, even though it actually broke even during the year. For most people, that negative income—even though it is NOT an out-of-pocket loss—will reduce their taxable income from other sources, like wages.

Even though cable television is full of programs showing people making supposed fortunes by acquiring houses in WA, fixing them up and “flipping” them, these programs are edited for entertainment, and they seldom show the whole story. Real estate works best when we hold it for a longer time frame to allow natural appreciation to do its job for us.

Like any investment, rental property ownership involves risk. Property values may not always rise as expected, rental income can fluctuate, and unexpected costs can affect returns. Considering downside scenarios in advance can help investors make more informed decisions and prepare for periods when an investment may not perform as planned.

Income-producing real estate requires some level of management. A successful landlord must be good at selecting tenants who will take care of the property and pay the rent on time. Owning one or more small properties may also involve repairs and maintenance.

While some choose to farm these kinds of jobs out, many landlords prefer to do the work themselves to save money. You should ask yourself whether you have the skills and temperament to do these tasks yourself. You may decide that hiring a management company is a good move. Having an experienced professional do the work for you could avoid a lot of problems, but be prepared to pay around 10% of the rental income for those services.

Owning rental property also means taking on legal and regulatory responsibilities. Landlords should understand that rental housing is subject to rules, requirements, and obligations that affect how the property is operated and managed. Taking these responsibilities seriously is an important part of treating rental ownership as a business.

We have given you some very general, simplified examples in this article. Before you make any decisions that are likely to have tax consequences, you should spend some time with a good tax advisor. They will be able to give you advice and information that is specific to your unique rental property situation.

For more information on the mortgage loan side of rental property ownership in WA, OR, ID, or CO, feel free to reach out to us, no obligation. Simply click the button below to get expert advice from our experienced loan officers.

Will you need mortgage financing to buy a home in Washington? We can help. Sammamish Mortgage has been serving buyers across the Pacific Northwest since 1992. We offer a wide variety of mortgage programs and products with flexible qualification criteria to borrowers across Washington, Idaho, Oregon, California and Colorado. Please contact us today with any financing-related questions you have, or visit our website to get an instant rate quote.

Rental property can be a strong long-term investment when it is chosen carefully, financed responsibly, and held long enough to benefit from appreciation, loan paydown, and rental income.

Leverage allows a buyer to control a property with a down payment and a mortgage. If the property increases in value over time, the owner’s equity can grow faster than the original cash invested.

Yes. Even if rent only covers the mortgage payment and operating costs, the property may still provide benefits through principal reduction, appreciation, and possible tax deductions such as depreciation.

Rental income and expenses are commonly reported on Schedule E. Taxable income is generally based on rents received minus eligible expenses, mortgage interest, and depreciation.

Depreciation is a tax deduction that reflects the building’s expected wear over time. For residential rental property, the building value is generally depreciated over 27.5 years, while land is not depreciated.

No. A paper loss from depreciation is a tax calculation and does not necessarily mean there was an out-of-pocket cash loss during the year.

No. Owning rental property also involves business responsibilities such as screening tenants, collecting rent, handling maintenance, tracking expenses, and complying with local laws.

That depends on the owner’s time, skills, and preference. Self-management can reduce costs, while a professional management company can handle tenant and property issues for a fee.

Professional advice can help a buyer understand tax treatment, financing options, cash flow expectations, and legal obligations based on the specific property and the buyer’s financial situation.

Yes. Investment property loans often have different down payment requirements, interest rates, reserve requirements, and qualification standards than loans for owner-occupied homes.

Our loan officers are ready and waiting to help you apply for your home loan.

Whether you’re buying a home or ready to refinance, our professionals can help.

Mortgage Support — 24/7

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

Adjust the parameters based on what you want to track