States We Lend In

Our loan officers are ready and waiting to help you apply for your home loan.

Many first-time home buyers have been shocked to discover that the amount of money they have to bring to escrow at closing is so large – especially when their loan contains an impound account. Let’s dig deeper into impound accounts and how they may affect the costs of buying a home.

The impound account – also called an escrow account – is money you deposit with the lender for the future payment of taxes and insurance. In addition to paying the principal and interest for the mortgage, you will pay 1/12 of the property taxes and homeowner’s insurance with each payment.

Lenders require this when the down payment is less than 20% of the purchase price, but most borrowers elect to have such an account even when the lender does not require it; the convenience of making just one payment each month, rather than setting aside cash for taxes and insurance is certainly attractive to many.

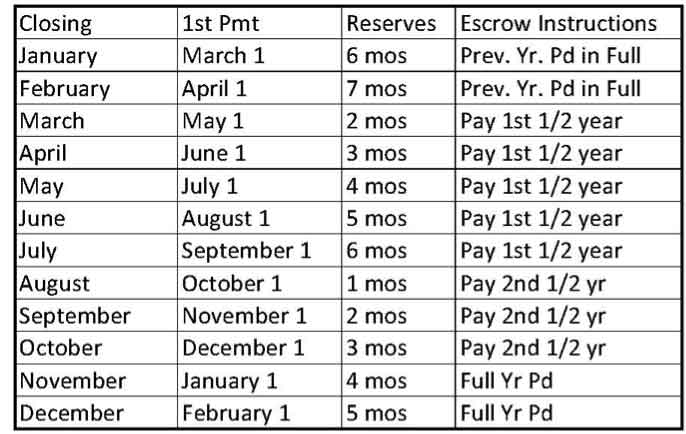

In order to create the impound account, you must make an initial deposit. This is called, “funding the impound account.” It’s still your money – it is just earmarked for taxes and insurance. The amount needed to fund the account depends on when you close escrow.

Property taxes in the state of Washington are paid on April 30 and October 30. Each installment covers one half of the total tax bill. The impound account must have enough cash in it so that there is still a two-month “cushion” remaining when it reaches its lowest balance during the year.

For example, if you close escrow in February, your first mortgage payment will be due on April 1. You will fund your impound account with 7 months property taxes, and the previous year’s taxes will have been paid. If you close in July, you’ll make your first payment in September and you’ll deposit 6 months’ taxes into the account. Escrow will make sure the previous installment has been paid.

You will also deposit a portion of your homeowner’s insurance premium. The exact amount needed will depend on the renewal date of your policy. Generally, you can subtract the months remaining before your policy comes up for renewal from 14 months to get the amount. In other words, if your policy is due to be renewed in 6 months, you’ll deposit another 8 months to set up your new impound account.

If you are refinancing and your old loan has an impound account, you’ll still have to set up a new account – but you will receive the balance of your old account about two weeks after you have paid off the old loan. Your current mortgage statement may tell you the balance in the account. If it doesn’t, just call the toll-free number to find out.

The initial deposit to your impound account is one of the closing costs that will appear on your closing statement. For a refinance loan, you may be able to add this amount to your new loan balance to avoid having to come up with cash at closing.

Will you need mortgage financing to buy a home in Washington State? We can help. Sammamish Mortgage has been serving buyers across the Pacific Northwest since 1992, including Washington, Idaho, Oregon, and Colorado. We offer a wide variety of mortgage programs with flexible qualification criteria. Please contact us today with any financing-related questions you have.

Our loan officers are ready and waiting to help you apply for your home loan.

Whether you’re buying a home or ready to refinance, our professionals can help.

Mortgage Support — 24/7

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

Adjust the parameters based on what you want to track