Hayden Mortgage Lenders

Want a transparent mortgage rate? You’ll need to work with a mortgage lender that has a reputation for transparency. This helps ensure the loan you get is right for you, not just the biggest one you qualify for.

* $800,000 | 30-Yr-fixed | Credit Score 800+ | 25% Down Payment

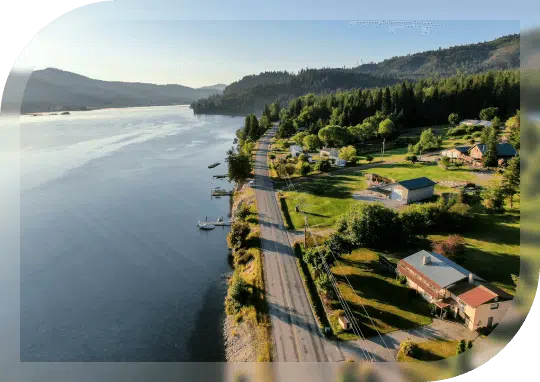

Nestled near Coeur d’Alene, Hayden, ID, offers the perfect blend of small-town peace and natural beauty. With stunning lake views, a strong sense of community, and access to year-round outdoor recreation, Hayden is a top choice for families, retirees, and professionals looking for a scenic yet connected place to live. At Sammamish Mortgage, we make it easy to secure financing in this appealing Idaho community.

Several factors come into play when determining your mortgage rate in Hayden:

Economic trends and market interest rates

The size of your down payment

Credit score and financial history

Loan type and repayment term

Total closing costs and lender fees

Our advisors will help you understand how these factors influence your rate and find the most affordable option for your unique financial profile.

For over 30 years, Sammamish Mortgage has delivered personalized lending experiences to homebuyers across the Pacific Northwest. Our deep industry knowledge, competitive rates, and responsive service make us a trusted partner in your homeownership journey.

Hayden offers a wide variety of homes — from cozy bungalows and lakefront properties to spacious new builds and family-friendly neighborhoods. Whether you’re a first-time buyer or upgrading your current home, Hayden provides both lifestyle appeal and investment potential.

Sammamish Mortgage offers a diverse selection of loan options to meet Hayden buyers where they are. Whether you’re seeking the reliability of a 30-year fixed-rate loan, taking advantage of VA loan benefits, qualifying for a low-down-payment FHA loan, or financing a higher-end home with a jumbo loan, we have a solution that fits your needs.

Want a transparent mortgage rate? You’ll need to work with a mortgage lender that has a reputation for transparency. This helps ensure the loan you get is right for you, not just the biggest one you qualify for.

Hayden borrowers have multiple loan options when it comes to getting their hands on a real estate loan. Here are some of the most popular home mortgage loan programs:

A 30-year fixed-rate loan is one of the most popular types of mortgages, since it lets you spread out the cost of buying a home in Washington for a reasonable monthly mortgage payment.

A 15-year fixed-rate mortgage features a fixed interest rate and consistent payments over a 15-year term.

ARMs are loans where the interest rate starts low and adjusts periodically based on market conditions.

VA loans are designed for veterans, service members, and surviving military spouses. Qualifying borrowers can get a home loan with no down payment.

FHA loans are designed for low-income or first-time home buyers who may not have perfect credit or a big down payment. You can achieve home ownership sooner than you think.

Jumbo loans can help qualify you to buy a home in a more expensive part of the country, even if the price of the home is higher than conventional loan limits.

Bridge loans refers to short-term financing that helps cover costs until long-term funding or a property sale is finalized.

Self-employment mortgages are designed for borrowers who earn income through business ownership or freelance work.

Bank statement loans use bank deposits as proof of income instead of traditional tax documents.

Asset-based loans are a type of financing that is secured by personal or business assets rather than just income or credit score.

DSCR loans are a type of investment property loans approved based on the property’s debt service coverage ratio rather than personal income.

1099-only loans are tailored for independent contractors who verify income solely through 1099 forms.

First-time buyer programs are Special loan options offering lower down payments or incentives for new homeowners.

Investment loans are a type of financing designed for purchasing rental properties or real estate intended to generate income.

Second home mortgages are designed for buyers looking to purchase a vacation property or secondary residence.

A Cash Buyer Program lets homebuyers make an offer without the usual financing contingencies required with traditional mortgages. With the Sammamish Mortgage Cash Offer Program, buyers can take ownership immediately and avoid the risk of paying high excise taxes that may apply when a title is transferred from a third-party purchaser.

The mortgage process begins with a conversation with a Loan Officer to review your financial profile, including income, employment history, assets, and credit. After submitting a mortgage application and the required documentation, your loan moves through processing and underwriting. Once all conditions are satisfied, the loan proceeds toward closing.

Mortgage pre‑approval involves a lender verifying your financial information to estimate the loan amount you may qualify for. It helps you focus your home search on properties within your budget and signals to sellers that you are prepared and organized for financing.

Homebuyers in Hayden can choose from a variety of mortgage programs. Conventional loans are widely used, while government-backed options like FHA loans provide flexibility in credit and down payment requirements. USDA loans may be available for eligible rural properties, and VA loans support qualified veterans and service members.

Closing costs typically include lender fees, appraisal and inspection charges, title and escrow services, and prepaid items such as property taxes and homeowners insurance. The total varies depending on loan type and local expenses. Your Loan Officer can provide a personalized estimate early in the process.

Lenders review your credit report and score to evaluate how you have managed debt over time. This assessment helps determine eligibility for different loan programs and terms. Reviewing your credit beforehand allows you to address potential issues or make improvements before applying.

Many mortgage programs permit documented gift funds from family members or approved sources to be applied toward your down payment or closing costs. Lenders typically require a gift letter and supporting documentation to confirm that the funds are a true gift and not a repayable loan.

An appraisal is an independent assessment of a property’s market value conducted by a certified appraiser. Lenders require appraisals to ensure the property’s value supports the requested loan amount. If the appraisal comes in below the purchase price, you and the seller may need to adjust the terms or explore alternative options.

An escrow account collects portions of your monthly mortgage payment to cover property taxes, homeowners insurance, and any required mortgage insurance. The loan servicer manages the account and disburses payments on your behalf when they are due.

Once your purchase agreement is signed, closing generally takes 30 to 60 days. This timeline includes underwriting review, appraisal scheduling, inspections, and title work. Providing documents promptly and maintaining clear communication helps keep the process on track.

Yes. Refinancing allows you to revisit your mortgage terms after purchase. This may involve adjusting the loan structure, switching to a different loan program, or accessing home equity for other purposes. A mortgage professional can guide you through the process and help determine if refinancing aligns with your goals.

Our loan officers are ready and waiting to help you apply for your home loan.

Whether you’re buying a home or ready to refinance, our professionals can help.

Mortgage Support — 24/7

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

Adjust the parameters based on what you want to track